Investment thesis on Alibaba Group

Calculated Risks for Compelling Rewards

Alibaba Group is commonly referred to as the “Amazon of China”. Like Amazon, it’s a leader in technology and e-commerce. Also like Amazon, it runs a conglomerate of ventures with their main pillars being e-commerce and the cloud computing segment. However, not everything is the same and the strategy employed between the two are actually quite different due to the geographical and cultural differences between the two companies.

Notably, our rationale for investing in Alibaba also differs greatly from that of Amazon.

One can’t really discuss the Alibaba story without talking about the macro environment in China. Chinese stocks have been in a slump since mid 2021. However, Alibaba’s decline from their all time highs actually happened even before that in October of 2020. Co-founder Jack Ma at the time ran into conflict with the Chinese government over a speech where he criticized Chinese regulators for stifling innovation. That was then compounded with the overall issues of government regulatory crackdown, the property crisis, geopolitical tensions, the Chinese government’s handling of Covid-19, and an overall slowing of the Chinese economy. All this has resulted in significant devaluation of all Chinese stocks including Alibaba. The main question we need to evaluate here is how much of a discount are we getting on Alibaba and is it sufficient to warrant the risks?

Note: Due to the similarity in structure, I will be referring to Amazon’s structure for comparison several times in this thesis. The investment thesis for Amazon was recently published and could help form a basis for better understanding Alibaba.

An overview of Alibaba Group

Alibaba Group is a conglomerate with a complex ecosystem. A brief breakdown of their segments are as follows:

Taobao and Tmall Group - This is the Chinese retail portion of the business. Taobao is a consumer to consumer marketplace sort of like eBay without the bidding. Tmall is the corresponding business to consumer platform that allows companies like Apple or Nike to sell to consumers.

Cloud Intelligence Group - This is the cloud computing segment.

Alibaba International Digital Commerce Group (AIDC) - AIDC is the international retail portion of the business.

Cainiao - This is the logistics focused portion of the business which includes things like warehousing, shipping, supply chain. Note that while Amazon ties the logistics together with their retail, Alibaba keeps this separate which means Cainiao can also work with other e-commerce platforms.

Local Services Group - This segment gets the award for the most uninspired name. It’s basically all the other services for consumers in China. Included in here is Ele.me which does food deliver (think DoorDash) and Amap which is a navigation focused app (think Google Maps). Broadly, Alibaba refers to these as Online-to-Offline (O2O) integration.

Digital Media and Entertainment Group - This segment is fairly self explanatory and has everything from user generated content on Youku to cinematic movies from Alibaba pictures.

All Others - This is the catch all bin for all the ventures that doesn’t fit into one of the existing segments.

Note that even this list is not comprehensive and only lists what they consider as “main businesses” and there are some smaller businesses that are left off like Koubei and Taoxianda.

In terms of revenue, all the segments contribute meaningfully in the TTM with Taobao and Tmall group (41.4%), AIDC - international commerce (11.1%), Alibaba Cloud (10.5%), and Cainiao - logistics (10.0%) taking the greatest percentages.

However, in terms of profitability, the Taobao and Tmall group is the primary contributor by far to EBITA. In Q2 2024 ending September 30, the group contributed 44.590 billion RMB to EBITA. The only other meaningful contributor is the Cloud Intelligence Group but at a much smaller scale of 2.661 billion RMB. The other segments are still in the growing phase towards profitability.

Of note, Alibaba presents their profitability measures by segment using EBITA as opposed to operating income like Amazon to add amortization back into the segments to account for a number of acquisitions they are making.

Let’s summarize some important takeaways from these numbers:

Alibaba is currently extremely dependent on the Taobao and Tmall group for profitable cash generation. Unlike Amazon where their cloud computing AWS contributes an outsized percentage to profitability, Alibaba is almost exclusively dependent on Taobao and Tmall. Because of the way Taobao and Tmall is set up, their margins are far better than Amazon’s e-commerce segment.

Alibaba’s Cloud Computing segment is likely to increase considerably over the next couple of years becoming a bigger contributor. The cloud computing segment just recently turned positive on TTM EBITA in December 2023 at 3.25 billion RMB. Three quarters later, the TTM EBITA of September 2023 is at 8.79 billion RMB. We expect a potential to double over the next year. While an imperfect comparison, AWS operating income grew from $0.5 billion in 2014 to $1.5 billion ( 3x) in 2015 to $3.1 billion (2x) in 2016.

Alibaba’s international segment (AIDC) is an unknown. Management has talked up the 29% gain in revenue YoY in the quarterly report. However, the cost of this growth is profitability. EBITA for Q2 2023 was -384 million RMB. In Q2 2024, it was correspondingly -2.9 billion RMB! To me, this is not impressive. Until management can show improvements on the bottom line, I view this as scaling up and not yet a proven business model. After all, this sector has intense competition.

The remaining segments are not particularly exciting.

Cainiao is profitable but as a logistics business with high competition and low margins, I don’t expect too much.

Local consumer services may be approaching profitability as they have been on a continuous trend of narrowing losses and in the most recent quarter reported an EBITA of only -391 million RMB. However, I don’t expect them to meaningfully contribute to Alibaba’s bottom line unless China’s overall economy improves dramatically.

The entertainment segment continues to trudge along at negative EBITA and doesn’t appear to be making any dramatic improvements. Luckily, it’s a small enough loss that it’s not too much of a drag.

The others segment generates considerable revenue contributing 18.9% of overall TTM revenue but a more in-depth review of the quarterly report shows that this segment’s revenue is direct sales revenue which is low margins like Amazon’s e-commerce business thus not likely to pass to EBITA. Furthermore, they’ve been hovering around 8 billion RMB losses TTM over the last couple of years and the trend does not appear to be improving rapidly.

Bottom line, Taobao and Tmall segment, Alibaba’s Cloud Computing, and AIDC are the areas we need to pay close attention to.

Valuation of BABA

Valuation is where Alibaba Group really shines. But how cheap is this leading commerce company?

DCF method: Alibaba has been increasing capital expenditure and investing heavily into the Cloud computing segment due to the AI needs since the beginning of this year

In FY2024 ending March 31, 2024, the FCF was 156.2 billion RMB, down from 171.7 billion in FY2023. I assume total FY2025 FCF to come in lower than FY2024 at around 120 billion RMB. Note this is more conservative than the Marketscreener analyst estimate of 133.1 billion RMB.

Because the macro environment in China is so uncertain, we explore both a pessimistic and an optimistic scenario.

Pessimistic Scenario: Let’s assume in the pessimistic scenario, China’s stimulus does not have any meaningful impact. Assume:

Further decline of 15% in 2025

Followed by very anemic growth of 5% for 2026-2029

Long term growth rate of 4%

9% discount rate (note some may adjust the discount rate higher for riskier investments but I prefer directly modeling a pessimistic scenario)

suggests an intrinsic value of the stock at $121.24. Note even in the pessimistic scenario, the stock is significantly undervalued.

Optimistic Scenario: Let’s assume in the optimistic scenario, the stimulus begins to have an effect in 2025 followed by accelerating growth over the next couple of years. Assume:

Decline of 5% in 2025

Followed by 10% growth in 2026, 15% in 2027 and 2028, followed by 10% in 2029

Long term growth rate of 4%

9% discount rate

suggests an intrinsic value of the stock at $171.37.

P/S method: Given several of Alibaba Groups segments are approaching but not quite at profitability. Price to sales methodology is an alternative way to evaluate intrinsic valuation. Given TTM revenue of $131.2 billion USD, 2.476 billion shares outstanding suggests an intrinsic value at P/S of 2.5 of $132.47.

P/E method: If we stick to using P/E valuation, we can use TTM EPS of $4.72, desired P/E of 20, and an assumed 10% growth next year to arrive at an intrinsic valuation of $103.84

In all 4 cases, the intrinsic valuation of the stock suggests the stock is significantly discounted at current prices. It’s worth noting the optimistic scenario presented is also a relatively mildly optimistic case. Averaging the 4 methods gives us a composite fair market value of $132.23.

Rationale for investment in Alibaba Group

Alibaba is a value play with considerable upside given the AI exposure. Even using the fairly conservative scenarios in the valuation section, Alibaba shows as undervalued. As the future impact of AI, China’s economy, their AIDC group, and cloud computing growth becomes more clear in future earnings calls, there will be an opportunity to update these. We review Alibaba as an investment based on my Criteria for Evaluating Stocks:

The company should be net income positive - Alibaba has been profitable for many years generating 79.7 billion RMB in FY2024, 72.5 billion RMB in FY2023 and 62.0 billion RMB in FY2022.

The valuation of the company must be attractive - As it is currently, I consider it a fair company at a great valuation. If Alibaba shows it is able to maintain it’s leadership in Cloud and Commerce through the next boom cycle of China, we may assess it as a great company.

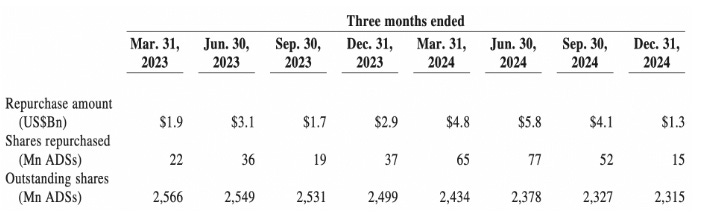

Shareholder friendly management - Alibaba Group deserves a lot of credit here. Their recent efforts in share buyback, total share reduction and changes in employee compensation towards more cash based incentives are all moves in the right direction to enhance shareholder value. The table below summarizes shares repurchased over the last 2 years.

Sector diversification and exclusions - Alibaba provides international (China) exposure. In addition, the Swan Select Portfolio currently only contains 2 consumer cyclicals: Alibaba and Amazon which is an acceptable concentration in this area.

Clean balance sheet - Alibaba’s balance sheet is stellar and they have a massive amount of cash with 183.0 billion RMB in cash as of Sept 30, 2024. (total debt-cash)/EBITDA ratio is only 0.29.

Risks: As always, it’s important to examine the flipside of the argument. In that respect, we highlight some key risks:

Taiwan Invasion - As tensions between China, Taiwan, and the United States has increased, this risk has become more real. I put this risk first as it will have by far the largest impact, not only to Alibaba Group but to all Chinese stocks. The exact magnitude of the impact is difficult to predict but certainly includes total loss, ie the entire investment dropping to 0. We do not believe this is likely to happen in the near term. A war of this scale would require large scale preparation that would be evident to the US through satellite imagery. Details of the rationale are beyond the scope of this investment thesis but are very nicely laid out in this article by John Culver, a retired CIA agent.

Heavy dependence on China’s economy and Taobao/Tmall segment - As we noted in the Overview section, Alibaba is heavily dependent on this segment until their Cloud Computing segment grows to sufficient profitability. This makes Alibaba particularly susceptible to the economic situation in China. Luckily, I believe the stellar balance sheet should help Alibaba weather any but the most extreme economic downturns.

Competition - In many ways, the competition in this sector is even more fierce in China than in the US. Multiple large companies such as JD, Tencent, and PDD are competing with Alibaba across multiple segments since the overall landscape is not as mature as in the US. In some ways, we need to depend on the scale advantage Alibaba currently has to ward off competition but we recognize this as a real risk that needs to be monitored. For now, I weigh this risk against the value proposition and find it still favorable.

Loss of focus - I had also previously mentioned this as a risk for Amazon. Alibaba similarly has many ventures and risks losing focus on their core profitable businesses. In some ways, this could be considered a bigger risk for Alibaba than Amazon because their core business has fiercer competition. Luckily, management has been selling some of these ventures recently to focus on core business which I believe is the right direction. Recent sales include Intime and Sun Art.

In summary, I believe Alibaba is a good investment when weighing risk/reward if purchased under $110 per share and is one of the stocks in my 2025 Swan Select Portfolio.

If you enjoyed the content, consider subscribing below. I also encourage you to take a look at my website BlackSwan Investor for other investing writeups.

Disclaimer: Any information contained here is not intended as, and shall not be understood or construed as, financial advice. I am not a financial advisor and this is only a documentation of my personal investment journey and decisions. You should always do your own research before making any final decision on investments.

Thanks for the write-up! I think Alibaba should get rid of those small and meaningless businesses and buyback more shares.

Great deep dive, BlackSwan!!!