Preliminary Prospects Series #2

A review of 4 promising investments with good potential

Dear Readers, this week, I’m really excited to bring you our Preliminary Prospects Series #2! Just like in Series #1, we try to cover a variety of the best companies in different industries and geographic locations with unique strengths that make them potentially great investments. If you haven’t already read Series #1, feel free to head over there and take a look after reading this one.

Also before we dive into the post, I wanted to share a bit of news. The Black Swan Investor newsletter has seen tremendous support over the last 4 months. Starting in April, we will be ending the early membership discounts for future paid subscribers and raising the monthly price to $15/month. If you’re finding good value in our newsletters and thinking about getting a paid subscription, it’s not too late to lock in the current price of $11/month. As always, anyone who signed up will keep their original subscription price for life.

In addition to the benefit of access to exclusive posts, paid subscribers also get access to live chat updates with my personal real time market trades and options activity. Make sure to take advantage of it!

Global Valuation Assumption: For all DCF valuations below, we assume 9% discount rate and 4% long term FCF growth rate after year 6.

Stock #1 Halozyme (HALO)

Most new drugs get approved based on being more effective for treating a disease. That can mean either helping you live longer or having less severe symptoms. However, another route to getting approval of new drugs is through offering more convenience. Halozyme’s proprietary technology does exactly this.

Imagine sitting in the doctor’s office with an IV attached to your arm for 4 hours at a time. Not a good use of time right? Unfortunately, some drugs could only be administered slowly so this was previously the only way. That’s where Halozyme HALO 0.00%↑ comes in. Their proprietary technology, ENHANZE, allows you to convert previous intranvenous (IV) treatments into a subcutaneous (SQ) treatment. Subcutaneous means “beneath the skin” which in this case means instead of sitting there with a needle slowly dripping the medicine into your veins, you can inject all of it into the fatty layer of tissue just beneath the skin and then wait for it to gradually absorb. The benefits of this are obvious, you can get up and leave. Typically, the downside is that absorption rate is poorly controlled but Halozyme’s ENHANZE helps with this. Result: no more sitting in the chair for 4 hours.

Now the reality is of course a bit more complicated. Each new drug using Enhanze technology needs to go through clinical trials, regulatory filing, and approval. This is why Halozyme only has two very simple drugs, Hylenex used for helping absorption and Xyosted used for testosterone supplement. The rest of their sales comes from collaborations with larger drug companies modifying their existing treatments to enable this more convenient method of delivery. In the short term, this is quite profitable as there are many existing drugs that can pair and take advantage of this.

Let’s take a look at the valuation of this company. The company’s FCF has grown quite solidly over the last 3 years from $235.3 million in 2022 to $373.3 million in 2023 to $468.4 million in 2024 while revenue has also grown by more than 20% in these years. Much of this recent growth has come from collaboration and royalty fees as we show in their breakdown of FY 2024 Financial Highlights.

Assuming FY2025 FCF of $500 million, 12% annual growth in FY2026-2029, and adjusting for an annual stock based compensation (SBC) of $50 million a year gives a DCF estimated intrinsic value of $88.27/share. On the surface, this makes the stock look quite discounted at today’s price and it can be quite tempting to take a position here. However, I’ve still been holding off on this investment for reasons I will outline in the conclusion below.

When we look at the cash flow generation of this company over the next few years, I’m actually fairly confident in their ability to generate this level of cash. In fact, I show above their Licensed Partner Product map that highlights sources of royalties and they look quite robust. However, my primary concern regarding this company is that they are a 1-trick pony. What happens when the patent for ENHANZE runs out in 2029? Would we expect their revenue to drop 30-50% over a period of a few years? If we model that scenario, the stock no longer looks discounted. They also do not appear to be throwing more money in to R&D to build out other pipelines of drugs.

My plan: For the reasons just mentioned, I’ve been keeping the stock on my watch list and carefully monitoring any conference presentations they are attending. If they show signs that they are developing something new and promising that fits within their expertise, I think that may provide a good entry point. The other aspect is if biotech as a whole starts to pick up further in merger and acquisition activity, I may consider picking up this stock as it could be a good acquisition target for one of the bigger pharmaceutical companies. Until either of these situations occur, I currently do not plan to open a position.

Stock #2 Zscaler (ZS)

The cybersecurity market is forecast to grow quite quickly at around 12% CAGR over the next decade. Compared to cybersecurity in the local environment, the cloud environment is even more complex due to the distributed nature and the shared responsibility model to enable cloud to function. And for that exact reason, that’s also where increasing number of cyberattacks are coming from. Zscaler is a company that leads in the Cloud cybersecurity space providing a Cloud security platform.

Zscaler ZS 0.00%↑ identifies themselves as the world’s largest any-to-any security cloud platform. Pictorially, they share a simple overview of how vulnerabilities through cloud can occur and the implications that leads to. In the figure below, they illustrate how the cloud introduces multiple vulnerability access points.

Zscaler instead acts as the switchboard to separate these interactions. With their global footprint, they supposedly deal with more than 500 billion interactions a day. The company also plays well into the evolving AI trend since increased use of AI leads to increased need of security for AI.

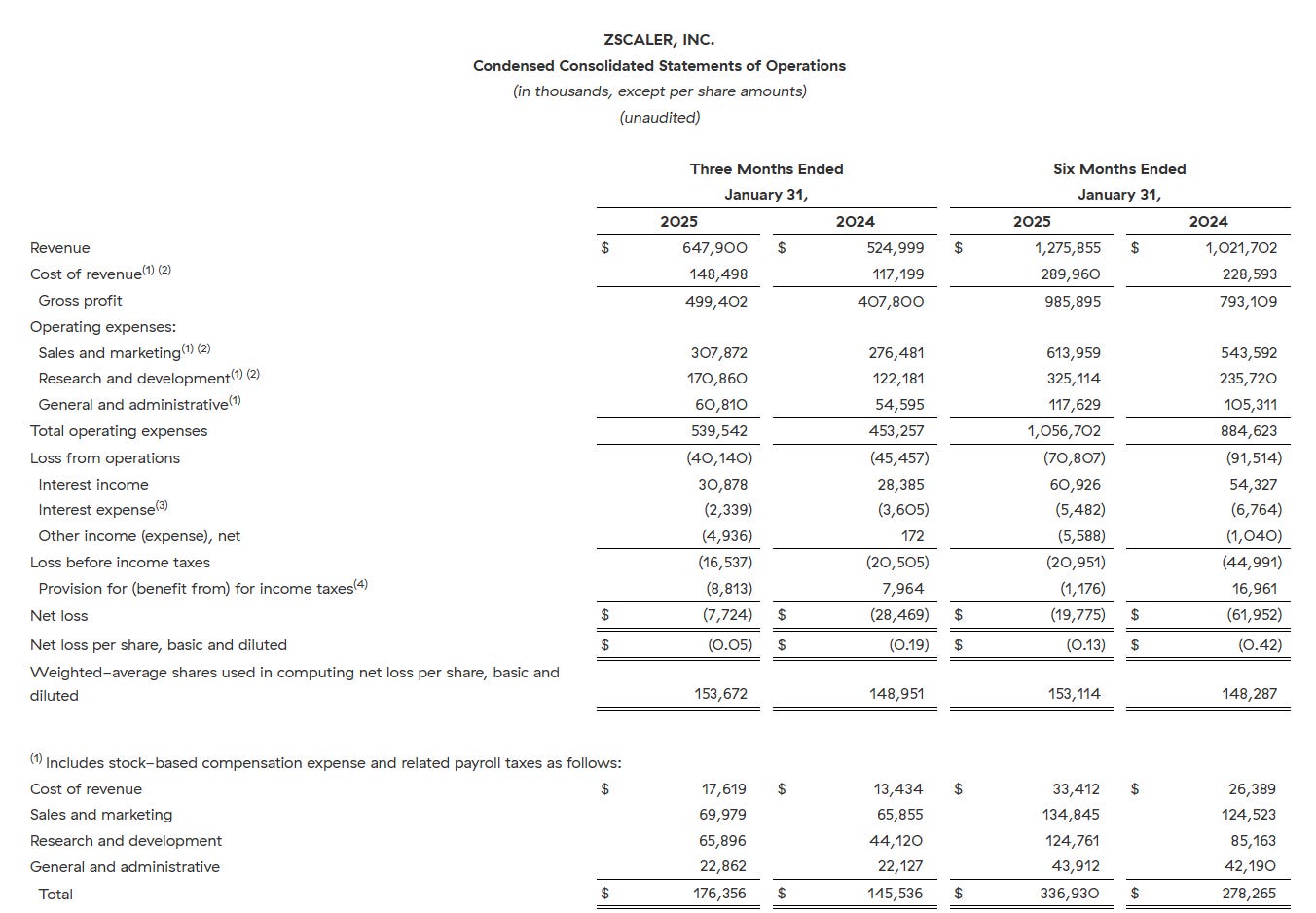

Now those that have read my Preliminary Prospects Series #1 will remember how much I like these enterprise SaaS (Software as a Service) companies as I talked about the advantages in brief when introducing Workday (WDAY). In addition to the built in Switching Cost Power, these companies also tend to be capital light and thus can generate ridiculous gross margins. In Zscaler’s case, they run gross margins at 81% over the last few years! Even in terms of free cash flow margin, they target around 22%-25% which is very impressive for a company expecting to grow revenue 22% next year. ($2.17 billion FY24 to $2.65 billion FY25)

Despite the excellent prospects for this company, there are key areas where the company is lacking which prevents me from opening a position. First, the company is not yet consistently net income positive. This is due to a combination of high levels of stock based compensation, relatively high cost of sales and marketing and increasing research costs. Now, I do not believe they are necessarily cause for concern as it reflects the competitive environment Zscaler is in. Typically, these issues should work themselves out as the company grows to larger scale. However, I will not personally invest at this early stage until they’ve established that they can manage these costs for a few quarters.

This is also one of the reasons I lay out Rule #1 in Criteria for Evaluating Stocks around positive net income.

As of the timing of this writing, ZS is valued around $197.81/share on the market. We assume based on the first 2 quarters that FY2025 FCF should fall around $715 million for the year. To justify this valuation using a DCF valuation basis would require us to assume around 22% CAGR from 2026-2030 and ignore stock-based compensation costs. I think achieving this level of growth is not unreasonable given their past performance and the secular tailwinds for the company.

My plan: I think Zscaler has a lot going for it and could offer considerable upside for investors with a riskier investment appetite. Alphabet’s recent purchase of Wiz shows how profitable such an investment could be. I wanted to highlight it here for this exact reason. Personally, I will stay disciplined by my own criteria and will continue to monitor this company to see how it grows in the next few quarters and would like to see better control on operating expenses and SBC before opening a position.

I hope you enjoyed the review of these 2 prospective investments. For paid subscribers, I provide 2 even better exclusive opportunities below. The next 2 prospective investments I review are at current valuations that I believe are already attractive and one of them is a natural monopoly!