Investment update on Amazon #1

Spending money to earn money, a review of Q4 2024 Earnings

Dear readers, Amazon released Q4 earnings on Feb 6th after the market close. Like all the big techs going into this earning season, the stock price dropped afterwards despite earnings and revenue beat. A quick search reveals articles attributing the drop to everything from slower cloud growth to Q1 outlook to increased capital spend.

To me, explaining why short term price movement occurs is the wrong question to address. The why is interesting and relatively easy to write about but it doesn’t directly help the investor. The more important and harder question is how much. Specifically, how much will material changes impact the ability for the company to generate profits and cash flow long term.

The latter question is particularly difficult given the many assumptions needed. Some may even argue that this is not worthwhile because these assumptions are often wrong. On this point, I would strongly disagree. Although assumptions can be wrong, they provide important context on impact. How do the events reported today change cash flow in the future?

After all, without this step, the investor is left with just a general concept and hope that the company should be more valuable in the future than it is today. And as we all know…

Hope is Not an Investment Strategy.

This is why in each investment thesis and update here, I aim to provide a Valuation section. In it, I will do my best to clearly lay out the assumptions and the corresponding impact ultimately leading to a fair market valuation. We regularly review these assumptions to update them based on the most current information. Consider subscribing if you believe this brings value to your own investment journey.

On that note, let’s also take a quick moment to discuss subscriptions. We are past 350 subscribers and I’m very thankful for the community we’re building here. I hope we continue to learn from each other. My intention is to always provide value for free subscribers interested in learning more about investing and as such, a good proportion of the posts will always be free.

However, if you’d like to further support me, consider upgrading to a paid subscriber and to show our appreciation, there are substantial additional benefits for this. In addition to exclusive investment ideas such as this post here, you also get early access to key investment updates. In this market, being timely can sometimes be as important as being informed. The recent Uber situation where the stock went up 8%+ the day after I posted our update to paid subscribers is an example.

The current subscription is $7.50/month and this will continue to increase until our target price of $15/month. Those who subscribe now will be locked in for life as a thank you for being early supporters of this newsletter.

Alright, that was a bit long so let’s move on to talk about Amazon and as a thanks for reading through all this, everyone will have access to this post immediately.

Amazon is a company we first reviewed about at the beginning of this year. At the time, we concluded it was a great company at a fair price at $210/share. The company is doing many things right but the price could no longer be considered discounted. I’ve included a link to the original thesis below.

Amazon has since updated their Q4 2024 earnings on February 6, 2025. Despite beating analyst estimates on both revenue and EPS, the stock has been down a few percent. Perhaps the biggest surprise for me this quarter was the announcement of the increased capital expenditure to over $100 billion for next year. Maybe this should have been expected after similar announcements by Google, Meta and Microsoft but the magnitude still surprised me. Let’s take a closer look to understand what how the earnings updates changes our investment thesis for Amazon.

Top Line Results

Let’s start by reviewing top line results.

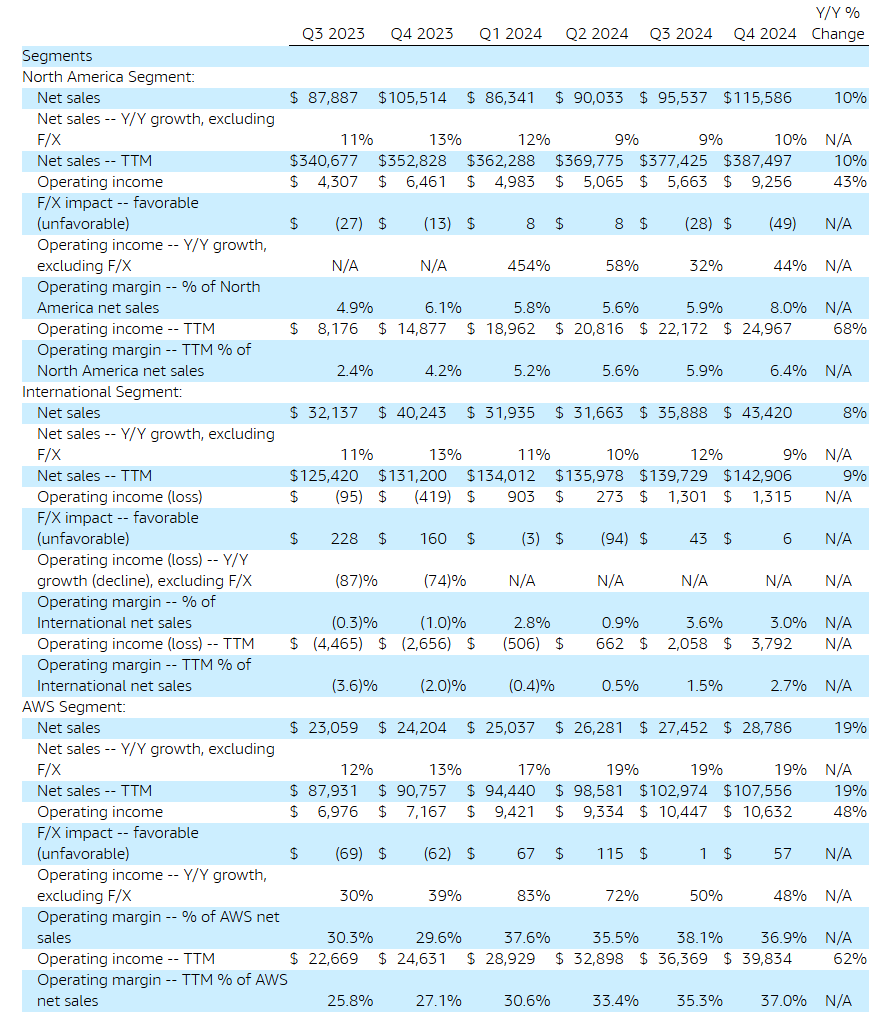

Q4 results show that AMZN 0.00%↑ net sales increased 10% YoY for the quarter to $187.8 billion and increased 11% for the full 2024 year to $638 billion. Further review of the segment breakdown do not show anything surprising. Growth in North America increased slightly from last quarter while growth in the international segment slowed slightly. The most important component is the 19% YoY increase in the AWS segment. This is a continuation of the acceleration we have been seeing for a few quarters now which is promising especially since this is the sector with the highest margins for Amazon.

Operating income increased to $21.2 billion, a 61% YoY increase in Q4. For the TTM, there was an 86% YoY increase.

Net income increased to $20.0 billion, an 88% YoY increase in Q4. For the TTM, there was an 95% YoY increase.

Operating cash flow for FY2024 came in at $115.9 billion which is a 36% increase from a year ago.

Free cash flow for FY2024 came in at $38.2 billion which is a 3.8% increase from a year ago.

As we can see, top line results look incredibly good for Q4 2024 and also for the entire FY2024. However, free cash flow continues to be constrained by the increased capital expenditure in FY2024.

Let’s take a closer look.

Review updates to our investment thesis

When we reviewed Amazon at the beginning of the year, there were 3 key aspects we found intriguing. Taken verbatim from our original investment thesis, they were as follows.

In summary, Amazon is an incredibly complex conglomerate to understand thoroughly. However, there are 3 key aspects that I believe defines Amazon’s story today.

Impressive cloud computing segment (AWS) with high net sales growth in a segment with high operating margins. This is the most valuable segment of Amazon currently and generates more operating income than all the rest of the company combined.

The e-commerce business continues to grow at a good pace around 10% annually and stands to benefit substantially from the introduction of AI. At the scale that Amazon operates here, even small improvements can lead to considerable profit gains.

The international segment may begin to contribute meaningfully to the bottom line starting in 2025.

Let’s assess each of these in turn.

The AWS segment continued to report high net sales growth of 19% YoY. Operating margins dropped slightly to 36.9% from last quarter but still remains quite high. I believe the AWS segment story remains intact.

The e-commerce business grew 10% YoY in North America and 9% YoY internationally in net sales which is what we basically expected to see. The North America operating margin to 8% was a nice surprise as I previously expected this to have plateaued around the sub 6% range. If this operating margin can be sustained at the 8% range, it would be a substantial increase to operating income given the large net sales base for e-commerce. Overall, the North America e-commerce business story came in better than what we previously assumed but we need to see Q1 results to verify if the higher operating margin is an anomaly.

The international e-commerce business seems to face some pressure but is heading in the right direction. We previously assumed this would reach around 3.5% operating margins in 2025 and this still seems reasonable. It has begun to contribute to the bottom line and the turnaround story remains intact.

All 3 of these aspects of the Amazon story for us are still intact. However, there is one additional aspect that has meaningfully changed. This is the increase in capital spend now projected to be over $100 billion. Previously, we had assumed the capex to be around $80 billion for FY2025. More importantly, capital expenditure has been regularly increasing from $52.7 billion in 2023 to $83 billion in 2024 to the expected $100+ billion in 2025.

To really understand what’s going on here, we dig into the numbers.

Capital Expenditure - Danger or Opportunity?

The increase in capital expenditure is an integral aspect of the Amazon story that needs to be addressed. Additional capital expenditure directly impacts our free cash flow and thus our valuation. However, there is a more fundamental question we need to answer first.

What’s the purpose of this increased capital expenditure?

Is this money spent for a massive opportunity to increase growth as all the big tech CEOs are saying?

Or is it an arms race to preserve cloud market share in the rapidly changing AI landscape?

Or is it perhaps a mix of both?

Obviously, it’s impossible to know the exact answer to this question but digging through the numbers provides what I believe is a reasonable perspective.

As with all inference problems, we need to first layout some underlying assumptions.

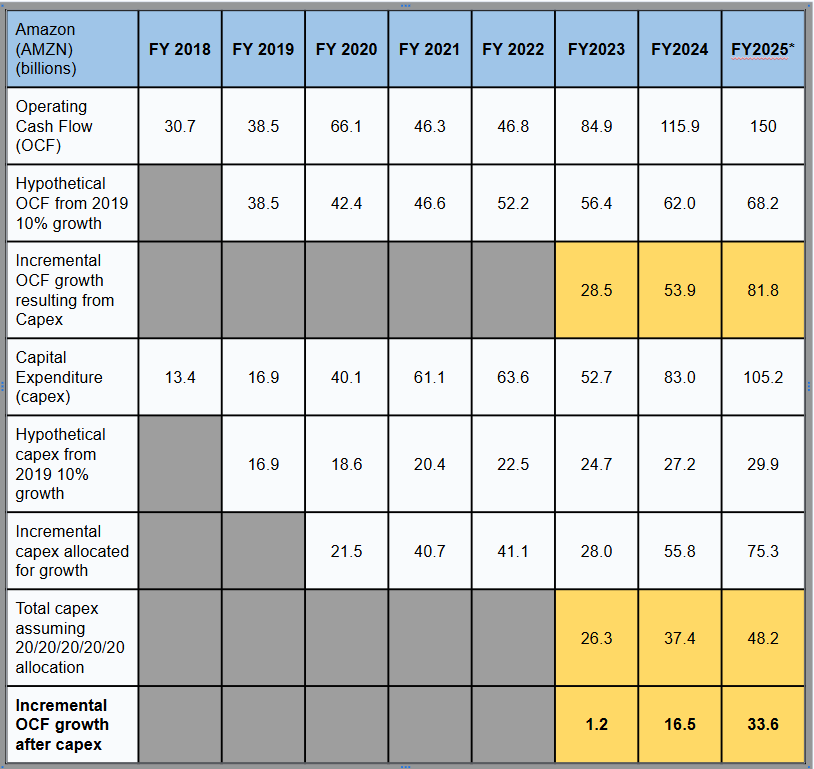

Amazon first significantly increased in their capex in FY2020 going from $16.9 billion to $40.1 billion. Let’s first assume if they did not begin massively increasing their capex, they could have maintained a base 10% growth rate in operating cash flow together with a base 10% annual increase in capex. We will call these the “Hypothetical OCF from 2019” and “Hypothetical capex from 2019”.

We also assume any capex spent on top of this base 10% growth rate is to improve the OCF growth of the company beyond the base 10% rate. We call this the “Incremental OCF growth resulting from Capex”.

Furthermore, since data center servers have around a 5 year useful life span, we assume the incremental capex allocated for growth has an impact that’s spread out evenly over 5 years.

Finally, we will assume FY2025 OCF is approximately $150 billion with $81.8 billion in capex spent. We share more details in the Valuation section on how we obtain these estimates.

Combining these simplified assumptions together allows us to approximate the additional growth in operating cash flow the company was able to obtain after accounting for the cost of the incremental capex spent for growth.

We call this the “Incremental OCF growth after capex”. A positive number here indicates that the money spent is worthwhile since it resulted in more money coming in than was spent to obtain it. A negative number here would instead indicate the spending was not worthwhile and the company may be spending just to fend off competitive pressure.

Interestingly, when we review these numbers we see that the Incremental OCF growth after capex is positive but only really start having a substantial benefit in FY2024. In fact, this was the first year where we start to see proof that the incremental spend may be worthwhile. Furthermore, only after FY2025 do we really anticipate to see stronger benefits.

This makes the next few years really critical. After all, if everything looks as we expect by the end of FY2025, Amazon would still have spent $262.4 billion capex to generate less than half of that ($111.9 billion) in operating cash flow. And that’s not even accounting for the discounted cost of spending cash upfront.

In summary, it appears that Amazon’s high capex is indeed targeted towards an opportunity for growth. However, the payoff is further out than I believe many investors realize and thus there remains substantial risk. Can Amazon continue generating these incredible levels of operating cash flow over the next 4-5 years to justify this capex spend? The current data seems to suggest yes but only time will tell.

Valuation of Amazon

DCF method:

For valuation, we follow the same methodology in our original investment thesis and first estimate the operating income. Operating income by segment for FY2025 are: $24.967 billion for North America, $3.792 billion for International, and $39.834 billion for AWS. For the North America segment, we expect 9% growth in FY2025. For the International segment, we expect roughly double the FY2024 operating income since only the last 2 quarters of this year contributed meaningfully. For the AWS segment, we keep growth expectation to 21% growth. This suggests revised operating income for 2025 should come in at $83 billion.

From here, we estimate the operating cash flow for 2025 by first adjusting the operating income for taxes (~15% for Amazon) then adding depreciation, amortization, and stock-based compensation and adjusting for changes in working capital. Depreciation and amortization is estimated at 55 billion. We approximate SBC will stay consistent around 23.3 billion. For simplicity, we also assume working capital will stay the same. Based on this, we estimate operating cash flow to be $148.85 billion. We round this to $150 billion for the Capital Expenditure section above.

Finally to get an estimate of FCF for FY2025, we subtract capital expenditure. Since management approximated FY2025 capital expenditure as similar to Q4 2024, we approximate as $26.3 billion x 4 = $105.2 billion. This suggests 2025 FCF should be around $43.65 billion. Although I previously modeled Amazon’s FCF for subsequent years using a projected growth rate of 30%, 25%, 20%, 15%, and 12% in subsequent years, the methodology becomes increasingly inaccurate due to how the company is spending capex as described in the previous section.

Instead, we assume

Capex spend drives operating cashflow to grow by 25% in FY2026, 20% in FY2027, 18% in FY2028, 15% in FY2029, and 10% in FY2030.

Capex spend continues to increase 10% annually from $105.2 billion in FY2025.

9% discount rate

long term growth at 4% after FY2030.

The first 2 assumptions equates to FCF of $70.34 billion in FY2026, $95.98 billion in FY2027, $123.44 billion in FY2028, $148.96 billion in FY2029, and $163.86 billion in FY2030. Under these assumptions, we arrive at an intrinsic value of $225.45.

In my previous post, I deliberated the appropriateness of accounting for stock-based compensation (SBC). After careful consideration, I believe it is appropriate to adjust for SBC as the most fair and accurate method. Further adjusting for $23 billion SBC annually to avoid dilution of shares, we get an intrinsic value of $189.22.

EPS method: EPS for FY2024 came in at $5.53. This came in higher than our previous estimates. Further assuming:

EPS growth of 30% (increased from 25% previously)

PE of 30

suggests an intrinsic value of the stock at $215.67.

To arrive at a final fair market valuation, we average the DCF method accounting for SBC and the EPS valuation method weighed 2:1 to arrive at $198.04/share.

Overall Summary

In summary, I believe Amazon remains a great company and their topline results for the Q4 quarter were overall excellent. The key aspects of our investment thesis has not changed but a combination of their increased capex spend, added risk over future FCF sufficient to justify this increased spend, and rise in stock price are beginning to push them into overvalued territory. For now, I continue to hold and monitor as great companies will often outperform expectations but will not accumulate more.

If this was interesting, consider subscribing and stopping by the BlackSwan Investor Main Page to see what other topics you may have missed.

Disclaimer: Any information contained here is not intended as, and shall not be understood or construed as, financial advice. I am not a financial advisor and this is only a documentation of my personal investment journey and decisions. It should be noted the author may own positions in the stocks discussed in this blog which could create a conflict of interest. You should always do your own research before making any final decision on investments.