Investment thesis on Tenet Healthcare

A healthcare services company with improving margins at a great discount

As we head towards the end of 2024, the market has been getting increasingly more expensive and overpriced. However, this increase hasn’t been uniform across all sectors with technology benefiting disproportionately increasing 67% in the last year. In response, I have been actively looking for opportunities in other sectors that may not have gone up as much this last year and thus may not be as expensive a valuation. The 2 previous investments I wrote about, Lantheus and Valero, were in such sectors with Healthcare up 17.5% and Energy up 12.6% respectively this last year. I plan to check back on this in a year to see if this was a good decision.

My latest investment, Tenet Healthcare, is a position I recently started that is also in the Healthcare industry. Specifically, this company has significantly improved their business in the last year and I believe valuation is discounted from this point today.

An overview of Tenet Healthcare Corporation

Tenet Healthcare operates a number of healthcare facilities mostly in the United States specifically in 3 segments: Hospitals Operations, Conifer Services, and Ambulatory Care.

Hospital Operations and Services - As of the end of Q3 2024, the hospital operations portion consists of 49 acute care and specialty hospitals, 142 outpatient facilities (imaging centers, urgent care, etc). The Services portion consists of Conifer Health Services which is a revenue cycle management and other value-based care services. These two segments were merged in their reports starting at the end of 2023.

The Ambulatory Care segment is comprised of the USPI subsidiary which holds indirect ownership interests in 520 ambulatory surgery centers (ASC) and 24 surgical hospitals. 161 of these facilities are noncontrolling interests. This segment is also the area that Tenet has been actively trying to grow as it both requires less capital and provides higher margins.

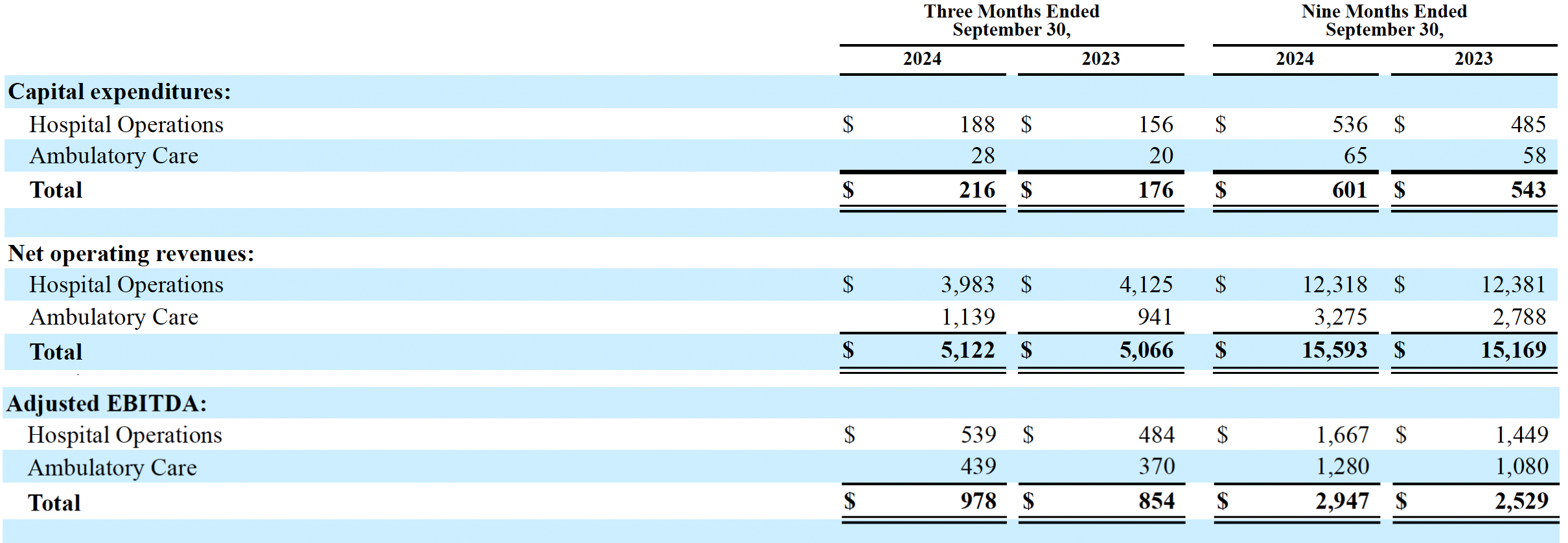

The following figure from the Q3 2024 Report shows clearly the value of the Ambulatory Care segment. In the last 3 months, Adjusted EBITA for the Ambulatory Care sector is 38.5% of net operating revenue whereas Adjusted EBITA for the Hospital Operations is only 13.5% of its corresponding net operating revenue implying Ambulatory Care is almost 3x the adjusted EBITA margins or Hospital Operations. Furthermore, capital expenditures as a percentage of net operating revenue is also about 50% cheaper in the Ambulatory Care segment. The fact that these margins stay fairly consistent between 2023 vs 2024 as management grew the ambulatory segment by 17.5% on net operating revenue based on previous 9 months shows this as a promising direction of growth. Management also highlighted their focus on higher acuity (more complex) cases which has also improved adjusted EBITA margins for the hospital operations.

Valuation of THC

Tenet Healthcare has dramatically improved cashflow and have been using this to pay down long term debt which has led to a significantly improved balance sheet. Since management has been divesting some less profitable hospital units, I conservatively estimate only modest FCF growth moving forward. Despite the slow growth, the stock is very attractively valued by both FCF and EPS methods. In reality, there maybe be additional upside given management’s directional shift towards more growth in USPI. Under the conservative valuation assuming next year free cash flow of 2.28 billion and assuming:

9% discount rate

Consistent and Longterm growth rate: 4%

suggests a fair stock price of $340.95 which is an enormous discount to the market close value of $133.77 as of 12/16/2024.

updated 2/15/2025 to remove 1 time recurring EPS charges in Q1 2024 and Q3 2024.

Using an earnings per share (EPS) approach, THC TTM EPS of $10.60. Assuming the following:

EPS growth rate of 5%

PE of 12

suggests an intrinsic value of the stock at $133.56.

Combined fair market valuation: To arrive at a final fair market valuation, we weigh the 2 estimates at 2:1 favoring the DCF method as it better accounts for long term investing value and arrive at a valuation of $271.82.

Rationale for investment in THC

Valuation: The large discount in the current market price is the biggest reason for this particular investment. Although there are some near term headwinds and potential uncertainties for healthcare and reimbursement changes starting next year, I believe the discount offered more than offsets these potential headwinds.

Low bar of growth in valuation: In our valuation, we only expect 4% growth moving forward. The overall hospital market is projected to grow ~3.5% annually through 2029. While this is not very fast, this in conjunction with operational efficiency measures management is implementing should make 4% FCF growth easily reachable.

Healthy balance sheet: The company has been doing a great job reducing longterm debt. From a total debt of 16.2 billion in Q4 of 2023 down to 12.9 billion in Q3 2024 all while EBITDA has improved from 3.66 billion in FY2023 to 4.03 billion in the TTM from Q3 2024. Meanwhile, cash on hand has increased from 1.23 billion in Q4 of 2023 to 4.09 billion in Q3 2024. This has lowered the (total debt - cash)/EBITDA ratio from 4.1 to 2.2 which brings it in line with my investment criteria. The balance sheet is particularly important in the current climate due to some of the uncertainties in policy for which the company may need to adapt financially.

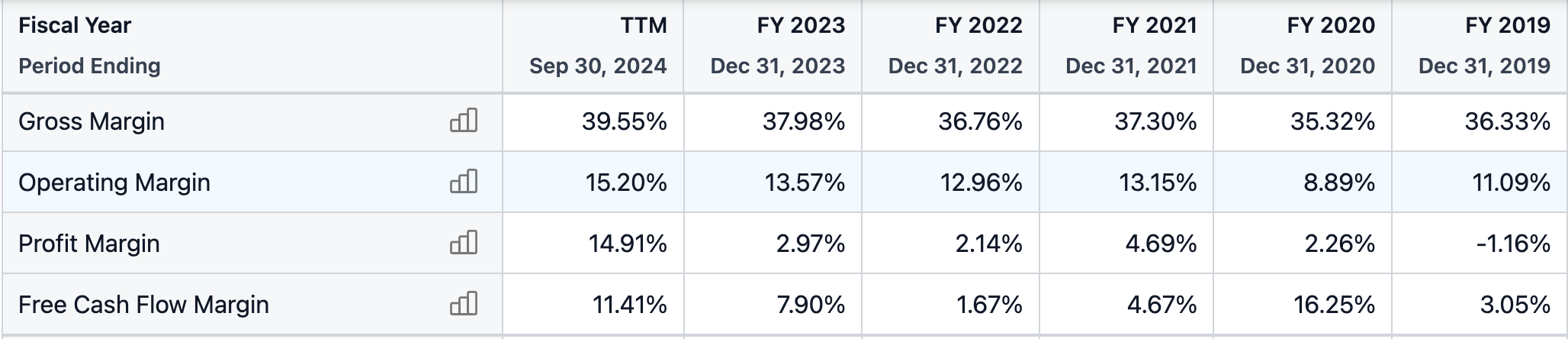

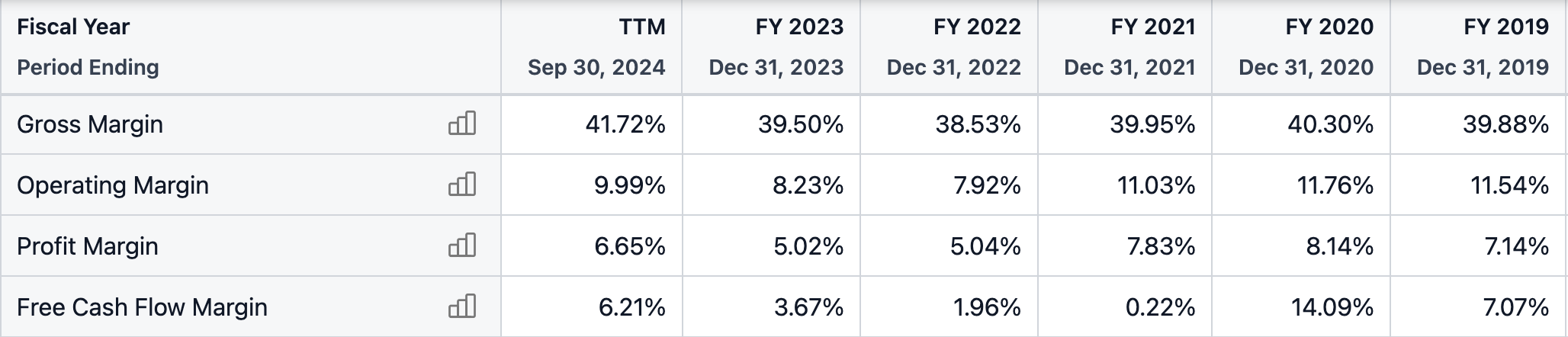

More efficient than the competitor: The summary below highlights that Tenet Healthcare has consistently been improving their operating margins. In addition, comparison between Tenet Healthcare and a comparable competitor, United Health Services (UHS), shows that Tenet Healthcare’s recent focus on acuity and their USPI subsidiary is clearly providing an advantage in margins. Having greater operating margins could be a notable advantage if policies change and reimbursements are reduced.

A summary of gross, operating, profit and FCF Margins for Tenet Healthcare (THC)

A summary of gross, operating, profit and FCF Margins for Universal Health Services (UHS)

Risks: The greatest risk for this investment is industry level. The hospital industry as a whole has been fairly inconsistent in FCF the last few years. This combined with the policy changes can provide considerable uncertainty in the near term and hamper short term price movement as has been highlighted by several downgrades by analysts recently. However, to me, the significant upside potential once the uncertainty clears up justifies the risk. Furthermore, the downside is somewhat buffered by the operational efficiencies shown by this company compared to its peers.

Overall, I’ve added Tenet Healthcare to my portfolio as a valuation play with relatively limited downside given it’s predicted free cash flow yield of ~ 17%.

Allowing for a 20% margin of safety based on the fair market valuation, purchases up to $226.52 per share are reasonable implying a significant discount.

Disclaimer: Any information contained here is not intended as, and shall not be understood or construed as, financial advice. I am not a financial advisor and this is only a documentation of my personal investment journey and decisions. You should always do your own research before making any final decision on investments.