Investment thesis on Qualcomm

A company in metamorphosis: growing beyond smartphones

When one thinks about Qualcomm today, the thing that likely comes to mind is smartphones. Although they own a whole range of products, they are probably best known for their Snapdragon processors and their wireless 5G modem technology. Founded in 1985, the company today is considered a semiconductor stalwart. Unfortunately, in recent years, the company has been plagued challenges and setbacks. Most notable among them has been the recent slowdown in the global smartphone market and falling out with Apple leading to the expected loss of a major customer.

However, it’s often when sentiments are low that opportunities can be found. Let’s take a closer look at whether Qualcomm is a compelling investment in 2025.

An overview of Qualcomm

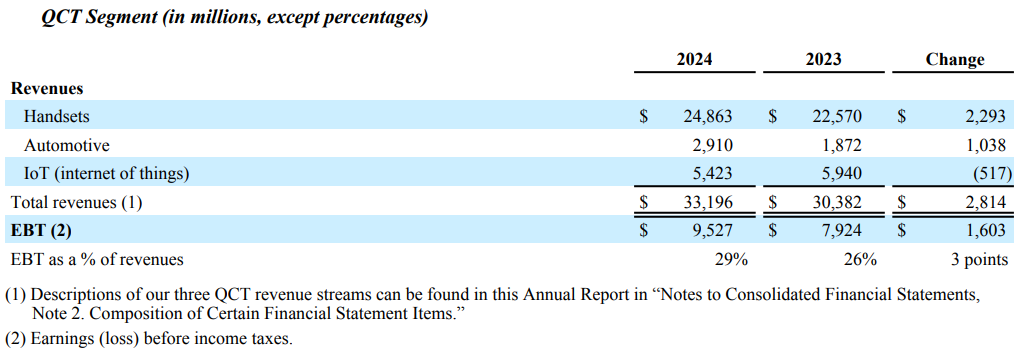

Although Qualcomm is best known for their chips in smartphones, the business is actually involved in many areas where wireless technologies are needed. As explained in their annual report, Qualcomm has 3 primary reporting segments:

Qualcomm CDMA Technologies (QCT) - This is the biggest segment and is responsible for developing and selling semiconductor solutions for wireless products. Revenue is divided into

Handsets which consist of Snapdragon processors and modems used in smartphones

Automotive which consists of chips and software for car including infotainment systems and autonomous driving

IoT (internet of things) which is just a catch all bucket for semiconductors used in all other devices like wearables, smart home devices, various devices used in commercial or industrial settings.

Qualcomm Technology Licensing (QTL) - This segment is responsible for licensing Qualcomm’s patents to other companies to earn revenue.

Qualcomm Strategic Initiative (QSI) - This segment invests in emerging technologies and startups and is the new technology side of the business. By getting involved, early, they can have a say in how Qualcomm products play a role in the future.

To put more simply,

QCT sells things,

QTL charges others for the right to make things, and

QSI works on new and exciting things for the future.

Within this company framework, it’s important to recognize Qualcomm actually has 2 main sources of revenue. It makes money as a semiconductor company selling it’s own chipsets but it also makes money from licensing it’s intellectual property to other OEM chipmakers. Although the QSI segment does not meaningfully contribute to revenue in the income statement, it is integral to driving long term value for the company.

A looming cliff of a problem

Of course, a close look shows why we associate Qualcomm with smartphones. In 2024, it was still $24.9 billion of the $33.2 billion revenue generated from QTL. This is also the big concern with Qualcomm. Several of their biggest customers have pulled away from Qualcomm. Notably:

Google has pulled away from using the Snapdragon processor in their Pixel phones since Pixel 6 in 2021 and instead are using their own Tensor chips.

Samsung has tried to move away from the Snapdragon processor but due to superior performance compared to their own Exynos processors, still retains the use of the Snapdragon processor in their flagship products.

Apple has been using their own A and M-series processors in their iPhones and are working on a transition plan to develop their own modems as well. While this plan has been delayed, it’s still expected to be completed by 2027.

Apple in particular is a headwind constantly looming over Qualcomm as they are estimated to still contribute around 20% of Qualcomm’s total revenue. Note the exact number is not reported and this based on analyst estimates. Assuming this is accurate, that would amount to around $6 billion in revenue lost in FY2027.

To add to this, Qualcomm’s licensing business has also faced both regulatory and legal challenges preventing it from growing.

It’s worth noting Qualcomm has not been sitting still in their core business. Knowing the direction of Apple, they have been shifting focus towards Android phones and achieved a 20% year over year growth in revenue in FY2024. However, this alone will not be enough to offset these losses.

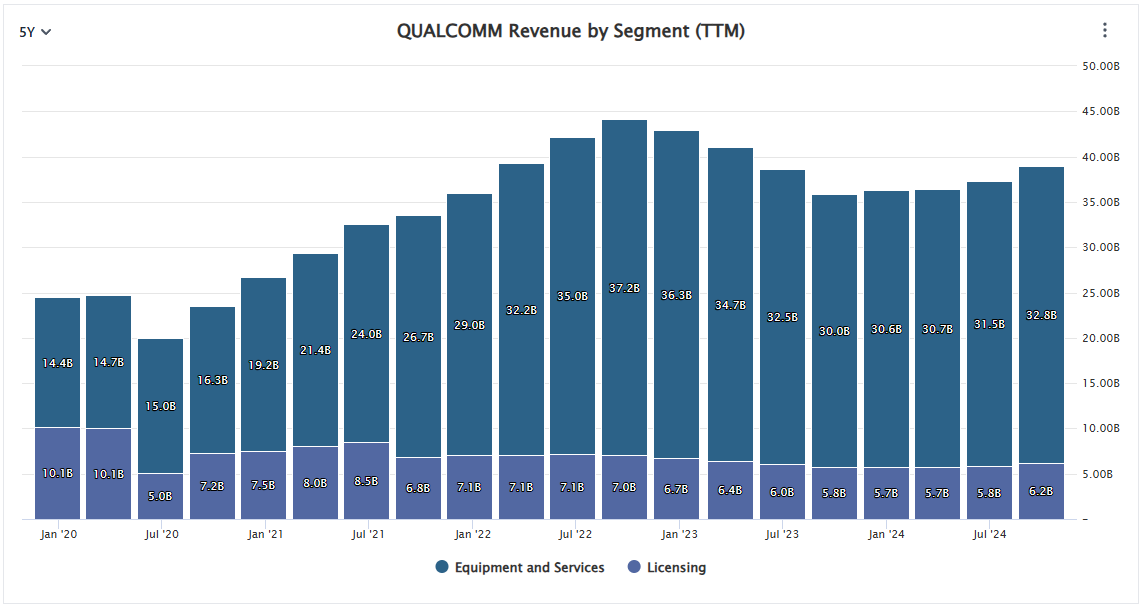

A summary of the revenue by segment below highlights the impact of these challenges.

AI - An opportunity of a decade

Now the good news, Qualcomm has had years of warning to adapt to these changes.

So what’s Qualcomm doing about this?