A primer on Dividend Stocks

Common Misconceptions and Strategic Use Cases

If you’ve been investing for any amount of time, you’ve probably heard mention of dividend stocks. Oh these stocks are wonderful, not only do you get the stock, you also get paid money every few months. It’s like buying a chicken and getting free eggs!

Or in my case, maybe it’s buying a swan and getting free eggs? In any case, let’s dive into dividend paying stocks.

Ok how exciting! but first… what are dividends?

When you buy stocks, you own a portion of the company. Some companies choose to periodically distribute the profits they make. One way to do this is through dividends. Basically, dividends are payments made by a company to it’s shareholders. Companies that pay substantial dividends (typically 2% or more) are commonly referred to as dividend stocks.

Now there are very good ways to utilize dividend stocks and I will review that at the end. However, I think the best way to truly understand dividends is through examining some common misconceptions.

Misconception #1 Automatically reinvesting dividends is the best way to compound returns.

Heard about reinvesting your dividends? You will often hear about this plan among dividend investors and on the surface it seems perfectly logical:

Buy stocks with great dividend yields

Collect dividends every 3 months

With the dividends, buy more of these stocks

Collect even more dividends!

Rinse and repeat, sit back, and continue benefiting from compounding growth.

But let’s examine it carefully. First, as a shareholder, always remember that you own part of the company. A very very small part but a part nonetheless! The dividends aren’t free money, they’re just giving you your own money. If the company can use this money well, they should be investing it to grow the company. After all, which owner doesn’t want a bigger company?

When the management of the company pays a dividend, they’re basically saying There are no places where the company can invest that is better than giving the money back to the owners.

And in the plan above, after management says they don’t have a great place to invest your money, you take this money and invest that money right back in the company by buying a larger share of ownership. Does that make sense?

To be completely accurate, this is in the ideal sense and reality is more nuanced. Sometimes, companies pay a dividend to get access to certain types of investors. For example, certain indexes or ETFs will only include stocks that pay a dividend. Nonetheless, it highlights the issues with the idea of reinvesting your dividends to generate compound growth.

Instead investing regularly in growth companies will more effectively create compounding growth.

But wait you say, dividend companies can be growth companies too! Look at Apple or Microsoft. First, these companies tend to have a fairly low dividend under 1% and are typically purchased for their growth aspect rather than their dividend aspect. Secondly, well this brings us to a another common misconception.

Misconception #2 Dividends are a great way to return shareholder value

Imagine your company generates so much free cash flow that it can support growth and paying dividends. Surely in that case, reinvesting dividends into the company is the best way to compound growth right? Actually, we’re still not being efficient. In fact,

dividends are not an efficient way to give money back to the shareholders.

The reason is the one word that strikes fear in all those who believe in the power of compounding, Taxes. Now the exact numbers will vary based on personal situation and the country you’re in but the concept remains the same. In the US, the tax rate for dividends can be upwards to 20%. This means every time you reinvest your dividends back into the company, you will lose up to 20% to taxes and only reinvest 80% of the dividends back.

This doesn’t sound like much but it really amplifies with compounding. If you had $100,000 and grew it by 10% every year, after 20 years, you’d have $672,750! But if you had to pay 20% taxes every year on those earnings, you’d only have $466,096. That’s more than $200,000 less!

So what’s a better way to return shareholder value? Stock buybacks! That’s when the company management takes their profits and instead uses it to directly buy and retire shares of the company. Alibaba Group which we recently wrote about is a company that has been heavily taking advantage of stock buybacks.

Stock buybacks achieves the same effect as reinvesting dividends but instead of everyone buying up a bigger slice of the pie, you just make the entire pie smaller.

The great thing here is that you don’t need to pay taxes since the company never distributed any funds. Warren Buffett, being the great investor that he is, recognized this early on which is why his company Berkshire Hathaway uses this exact strategy and doesn’t pay a dividend. Famously, Buffett also shared his thoughts on dividends with his shareholders during his 2012 Berkshire shareholder letter on pages 19-20.

In this spirit of accuracy, it’s worth noting the US government has also recognized this little loophole and Biden in 2023 added a 1% excise tax on stock buybacks but even with this addition, it is still far superior to dividend reinvesting.

Misconception #3 Higher Dividend Yields are better

This bring us to the third common mistake with dividend stocks. Searching for ever higher yields. After all, if a company paying 3% dividends is good. Surely a company paying 6% is better. And 12% even better right?

Unsurprisingly, this is not true. The crux of the issue here which I had previously mentioned is that

The dividends are not free money, they’re parts of the company you own being given back to you.

When the dividend yield is too high, it could mean the company is spending so much of their resources providing the dividends they may have enough to run the operations of the company itself smoothly. This is why monitoring a metric called the dividend payout ratio is important which is simply the percentage of total net income (profits) paid out as dividends. Valero is an example of a company we previously reviewed that has consistently managed their dividend payout ratio effectively.

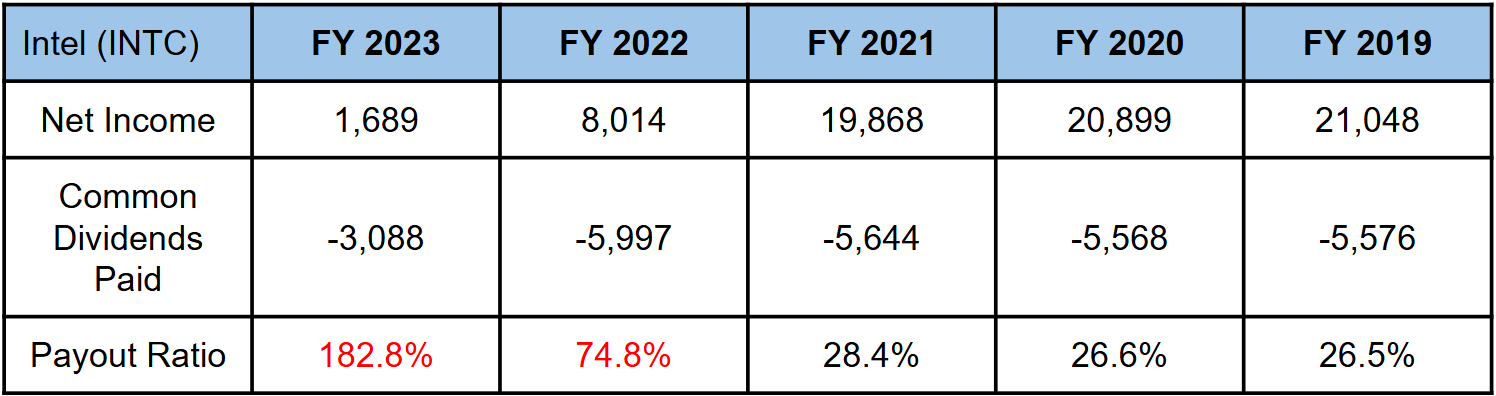

In some of the worst cases, companies may even borrow money to pay dividends to maintain consistent dividend payouts. This is a clear warning sign of financial instability and should only exist for a short duration. When you think of it from the owner mindset, you can clearly see why this is bad. Intel for example, continued to pay dividends even when they needed that money to reinvest in their future leading to a significant run up in debt before finally eliminating their dividends.

Updated 1/25/2025, with details on this example.

Let’s look at the Intel example more closely. First, we review the Cash Flow Statement to understand how much cash was paid out as dividends over the last 5 years.

Now the astute investor will immediately notice a problem. The payout ratio was gradually creeping up and in FY2022, it jumped massively to 74.8%. More dangerously, by FY2023, it jumped to over 180%. That means there wasn’t enough profits even pay the dividends much less anything else!

So how was this being funded? To answer that, we need to look over at the Balance Sheet. Now there’s a number of debt measures you could look at but the simplest is to just look at Total Debt or Total Debt - Cash.

The answer now becomes apparent. Intel has been borrowing money to pay for all their activities since they were not able to generate enough money on their own. In fact, if we are careful in digging through this, we would notice these changes even before the payout ratio impact.

I hope this helps elucidate some of the issues highlighted above with unsustainable dividend yields.

It’s worth noting that there are some class of companies such as REIT’s that are required by law to pay the bulk of their taxable income as dividends to benefit from certain tax benefits but that’s a discussion for another time.

So when should we own dividend stocks?

As I mentioned at the beginning, there are still very good use cases for dividend stocks. The key was to understand what they are not. Some appropriate uses for dividend stocks include:

As an income generation tool either in place of or combined with fixed income assets like bonds. For those that require a regular influx of money to cover expenditures, dividend stocks can serve this purpose. Although not as safe or consistent as fixed income assets like bonds, you do benefit from the growth potential that comes from owning stocks.

As a more defensive position to balance a stock portfolio. Dividend paying stocks tend to be more mature companies that have a steady stream of income. Furthermore, if a company has a consistent dividend yield for years, any downward pressure on their stock price is somewhat protected by the corresponding increase in their dividend yield rate. As a result, these dividend stocks tend to be more defensive positions in a stock portfolio and can help stabilize the ups and downs of a portfolio. This was also one of the factors considered when choosing the composition of our Swan Select Portfolio.

As an investment option in tax-advantaged accounts. Remember earlier when we talked about the implications of taxes when dividends are paid out? That becomes a non-issue in tax advantaged accounts like an IRA or 401k. While this alone shouldn’t be the primary reason, it does improve the overall desirability of dividend stocks in these accounts relative to a taxable account.

In summary, dividend stocks have a place in many well balanced portfolios. However, it’s not the amazing “does everything” product it is sometimes advertised as. The dividends themselves are reducing the assets of the company and come at a cost. Going back to our original analogy, when you buy the chicken, you don’t get the eggs free. It’s more like growing a lettuce and regularly cutting some leaves off. (I thought about staying with the chicken analogy but it got too morbid.) And on that note…

If you enjoyed this content, consider heading over to our Investing Academy to learn about other investing topics.

Disclaimer: Any information contained here is not intended as, and shall not be understood or construed as, financial advice. I am not a financial advisor and this is only a documentation of my personal investment journey and decisions. You should always do your own research before making any final decision on investments.